A closer look at buyer trends, enquiry activity, and lead performance across Victoria during the third quarter of 2025 reveals a market displaying renewed confidence and steady intent. Supported by improving lending conditions and consistent demand for new homes, buyer activity remains above the annual average across most key indicators.

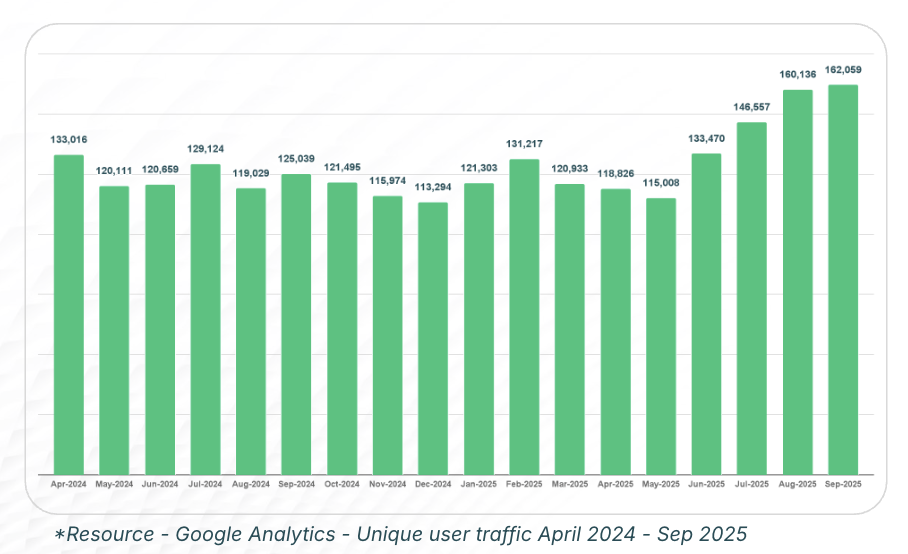

Unique Audience Trends

Victoria’s unique audience mirrored the national growth trend in Q3, contributing to a record-breaking 162,059 users across OpenLot nationally in September, a 21% lift from the end of Q2. The increase underscores heightened buyer confidence and renewed interest in greenfield opportunities as market sentiment continues to strengthen.

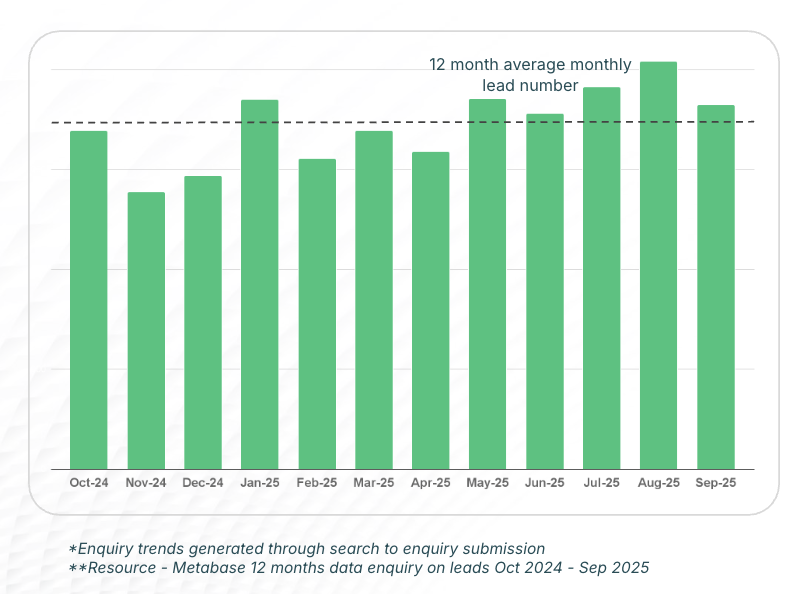

Enquiry Trends

Enquiries in Victoria remained robust throughout Q3 2025, with July, August, and September all surpassing the 12-month average. August in particular achieved the highest enquiry level of the year, buoyed by positive media sentiment around rate stability and government-backed housing initiatives, clear signs of buyer confidence returning to the market.

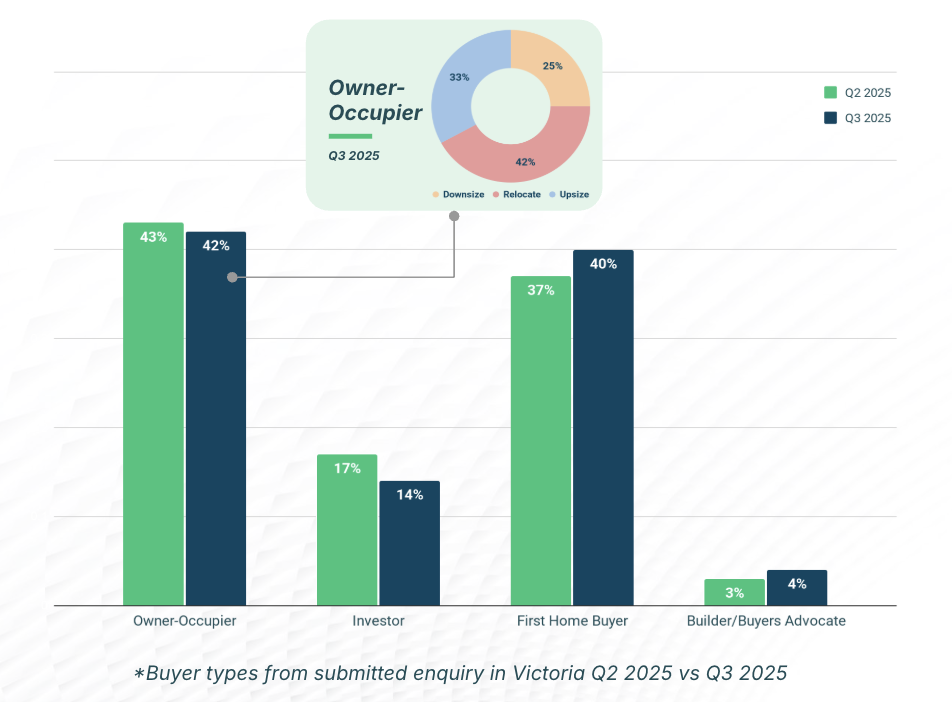

Buyer Types

Owner-occupiers remained the largest segment, accounting for 48% of enquiries, followed by first-home buyers at 37% and investors at 14%. Builder advocates represented a modest 1%, signalling a continued preference for personal occupation and long-term ownership.

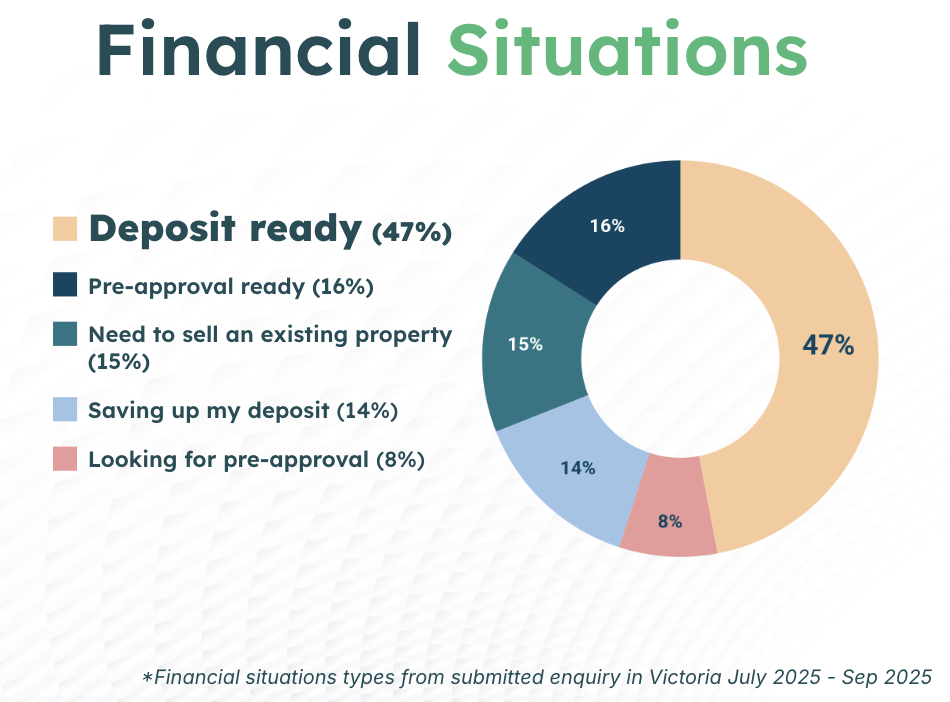

Financial Situations

Almost half of all enquirers, 47%, were deposit-ready, while 16% had pre-approvals in place. A further 15% were waiting to sell existing properties, and 14% were still saving their deposits. Only 8% were in the early pre-approval stage, indicating an increasingly finance-ready buyer pool.

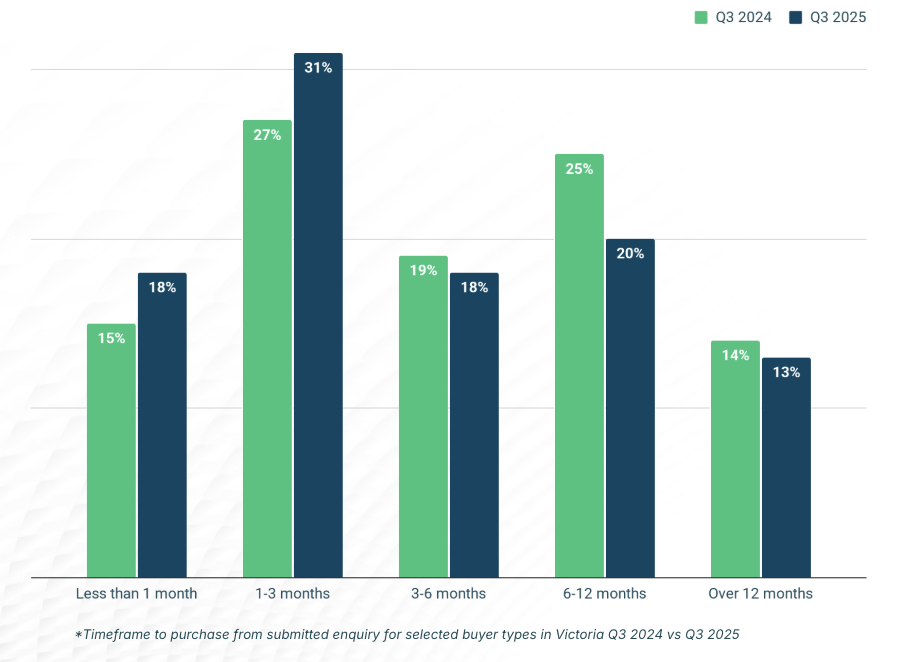

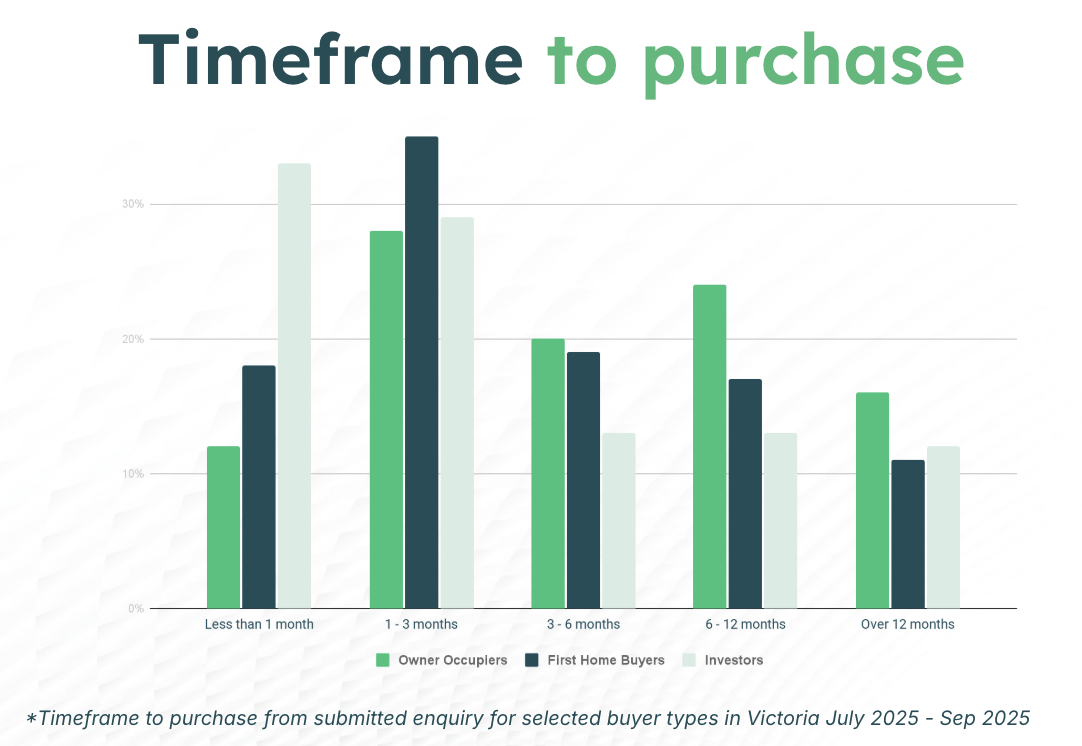

Timeframe to Purchase

Compared to Q3 2024, a larger share of Victorian buyers now plan to purchase within 1–3 months, 31%, up from 27% a year ago. This short-term intent highlights increased decisiveness among active buyers. Another 29% intend to buy within 3–6 months, while 26% expect to transact in 6–12 months. Only 14% report a timeline beyond 12 months.

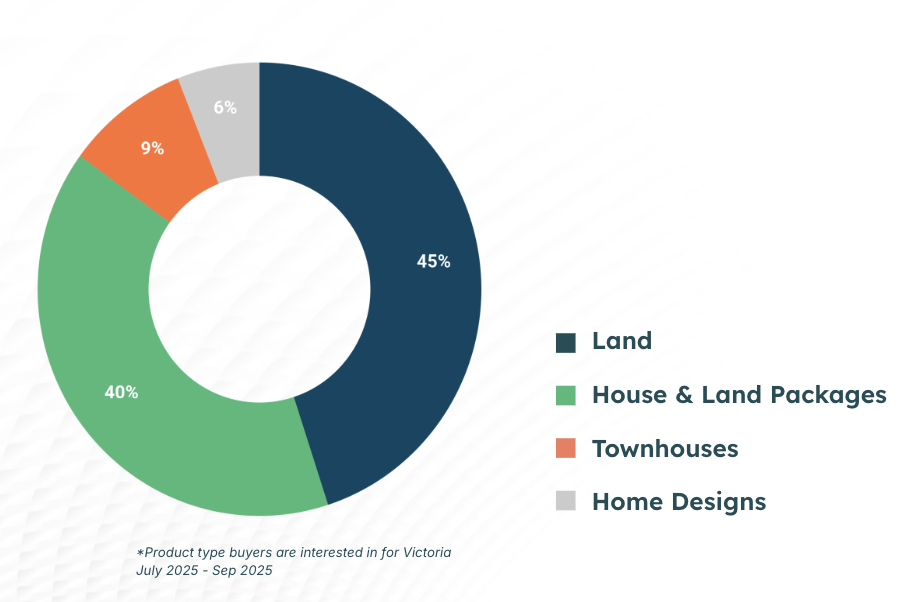

Product Demand

Interest remained evenly distributed between land, 45%, and house-and-land packages, 40%, with townhouses, 9%, and home designs, 6%, accounting for smaller shares. The strong land and package demand reflects Victoria’s enduring preference for build-new opportunities.

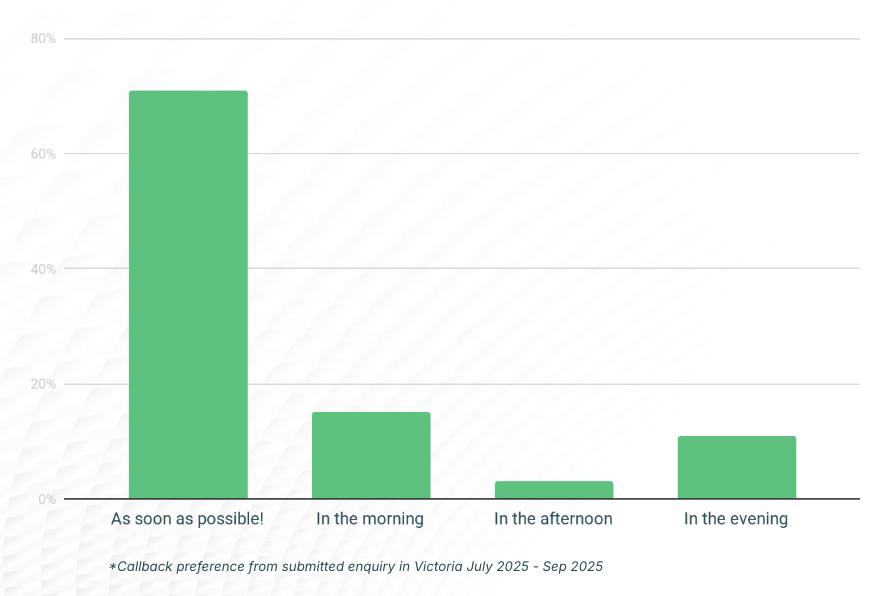

Buyer Callback Preference

An overwhelming 70+% of buyers requested to be contacted as soon as possible, far exceeding those preferring morning or afternoon calls. The immediacy of response expectations underscores the importance of fast follow-up for successful lead conversion.

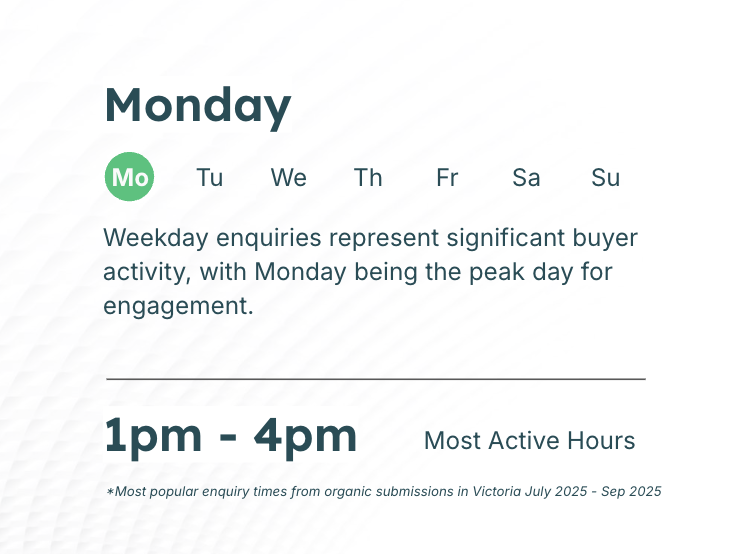

Most Popular Enquiry Times

Activity was heavily concentrated during weekdays, with Monday emerging as the peak day for engagement. The most active hours were between 1 pm and 4 pm, suggesting that buyers prefer to enquire during business hours, a key timing insight for sales and marketing teams.

Lead Maximiser Insights

From 2,489 leads called, 1,170 were successfully connected. Of those, 20% had already purchased, while 10% had bought established homes. A key insight: 10% of buyers reported no contact from sales agents, emphasising the ongoing importance of timely follow-up in lead nurturing.

Buyer Survey

Barriers to Purchase:

• Waiting to sell an existing property or access funds

• Rising land and construction costs

• Concerns about build quality

Preferred Products:

• Owner-occupiers: Established and new homes

• First-home buyers: New homes

• Investors: Established homes

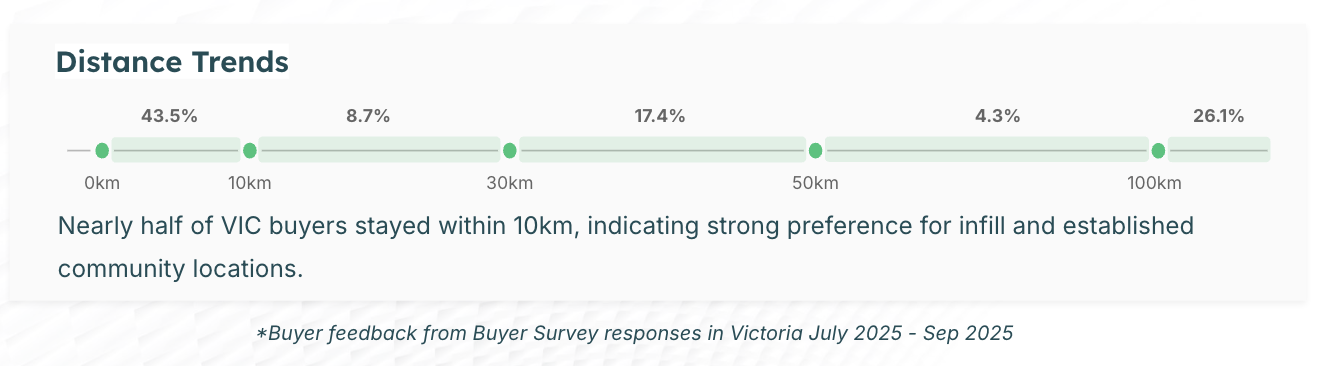

Distance Trends:

Almost half of VIC buyers, 43.5%, purchased within 10 km of their previous address, confirming strong preference for infill or established community locations.

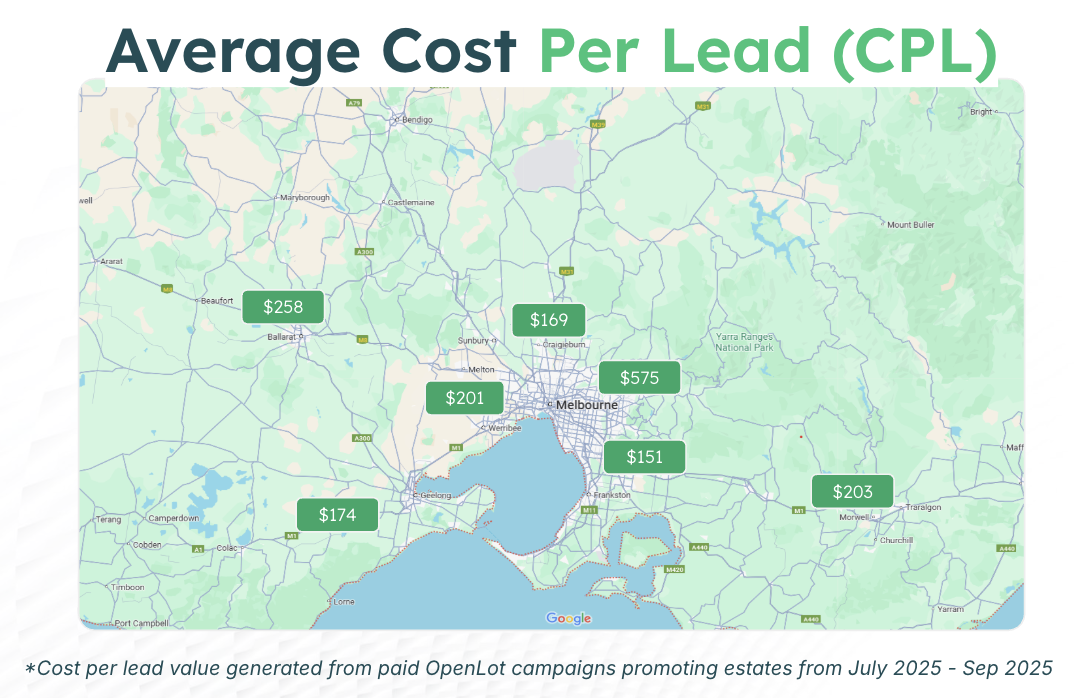

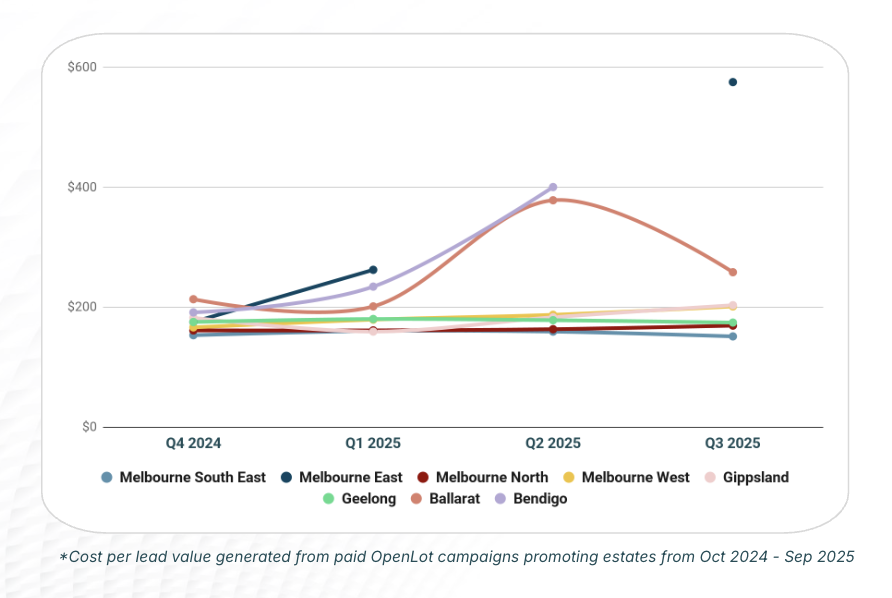

Average Cost Per Lead (CPL)

Across Victoria, paid campaigns achieved regionally competitive CPLs:

• $174 (West), $258 (North), $201 (South-East)

• $169 (Geelong), $151 (Bendigo), $203 (Gippsland)

Metropolitan regions such as Melbourne West and Melbourne North remained slightly higher due to stronger competition and higher buyer activity.

Victoria’s Q3 2025 market demonstrated consistent engagement and a notable shift towards purchase readiness. With strong enquiry volumes, an active weekday response pattern, and a buyer base increasingly prepared to transact, the outlook remains positive for both developers and builders heading into Q4. Strategic, rapid engagement remains key to capturing this motivated audience.